Demand on EM assets hits record due to carry trade. The note focuses on the most appealing ideas with the bulk of issuers rated BB or lower. Most of trade ideas for EM eurobonds market relate to Mexico, primarily to banking and O&G sectors. The most profitable issuers across EM come from Mexico, South Africa, Russia, Columbia, Indonesia, Oman, the most overweight — in Brazil, Hungary, China, Korea and Chile.

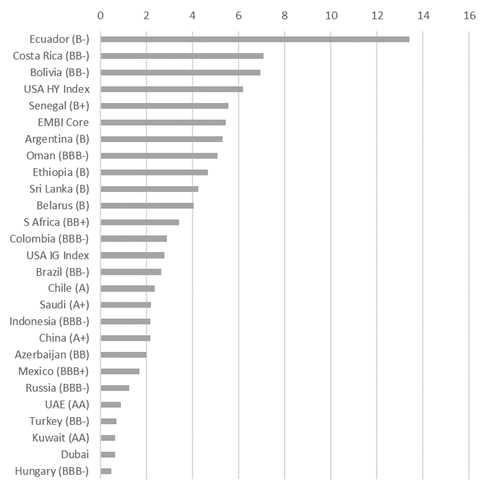

Sovereign Eurobonds, price change, ytd, %

Source: Bloomberg, ITI Capital

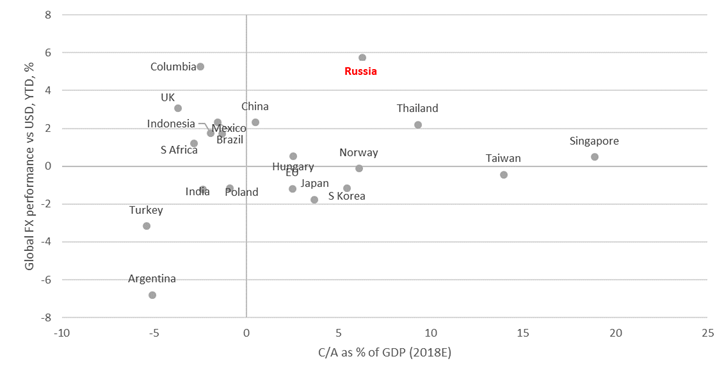

Russia: As good as it gets/Limited upside due to high country risks

For Russian sovereign USD issues, the yields have dropped to the lowest since late July, spread could narrow further by 25-30 bps, or 2% rise in price, if they come back to the presanctions (Rusal) benchmark levels. With than in mind, average upside potential among corporates is 4%. VTB’s upside is 6–8% depending on duration, Alfa’s and VTB perp’s — over 8%.

With respect to August levels (EM sell off and announcement of second round of sanctions against Russia), sovereign bonds’ upside is limited around 1%, the corporates’ upside is 2%. Alfa and VTB perp upside is 5–6% due to high risks. Hence, most of Russian issuers have approached July levels.

Importantly, the current 5Y CDS is only 10 bps lower than the level seen prior to sanctions against Rusal and therefore does not reflect the country risk premium. Russia’s sovereign bonds price is justified if compared to that of their peers.

The current risk premium prevents corporates including financials’ yields from edging lower, especially amid imminent sanctions that will likely hit primary OFZ market. With non-residents holdings accounting for 45% of sovereign eurobonds (CBR data) market and 60% (our assumption) of corporate bonds market, the upside potential largely depends on geopolitics.

Source: Bloomberg, ITI Capital

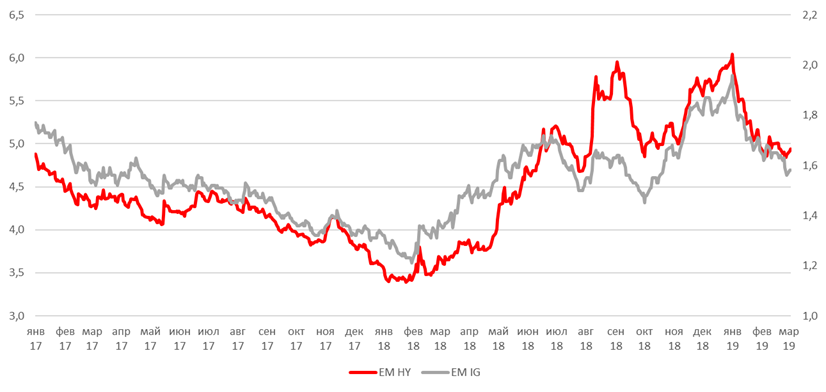

High yield junk bonds are back

FX-denominated securities below investment-grade (from ССС+ to ВВ+) have enjoyed the strongest demand year-to-date. Hence, junk-rated securities’ yields dropped by 100 bps to 4.9% due to overall demand on risky assets and overweight EM debt in 2H2018, according to Bloomberg Barclays High Yield Index. Importantly, yields of many investment-grade securities (from BBB- to ААА+) have approached the lows and stand at 2%, according to Bloomberg Barclays Investment Grade Index. Securities issued by countries offering risk premium, such as sanctions-hit Russia (BBB-), are an exception.

International sovereign yield curve, %

Source: Bloomberg, ITI Capital

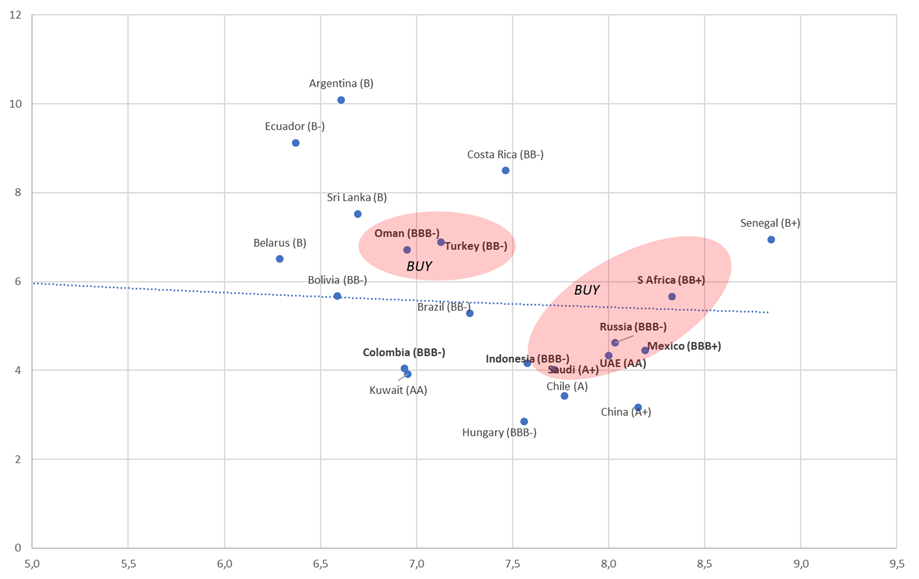

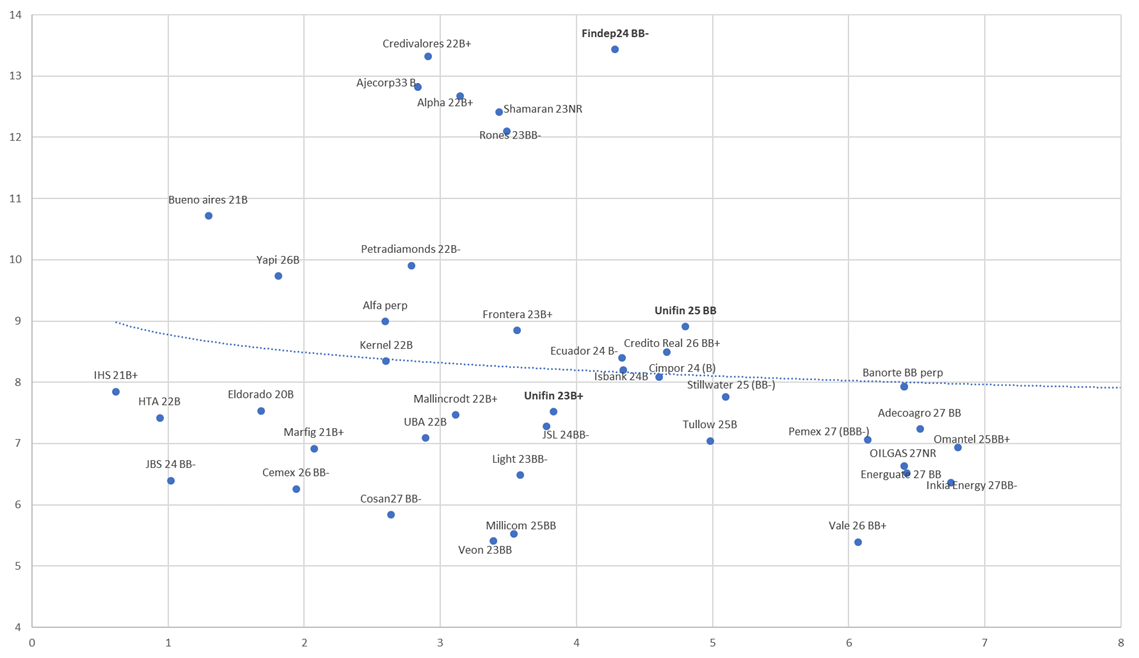

Yield misplacement of leading EM Eurobond issues

Given that some countries such as Russia, Mexico, the Gulf states (Saudi Arabia, Kuwait, Oman etc.) carry specific risks, while other countries such as Brazil are back on track for further growth, the debt market underwent a positive revaluation resulting in a shift towards lower grade FX-denominated bonds. For example, Brazilian (BB-) securities have been trading closer to investment-grade level and those considered the most overvalued. The narrowest spread between Brazil’s debt and investment grade securities with similar duration is 100 bps, while historically it was 150 bps. When it comes to Petrobras (BB-) and Gazprom (BBB-) bonds, the current spread is by 60 bps narrower than historical one due to excessively strong demand on the Brazilian securities.

Bonds issued by Russia, Mexico, UAE, Indonesia, South Africa and Saudi Arabia that offers risk premium over the assassination of a Saudi dissident and WSJ journalist Jamal Khashoggi, are among the most underweight securities. Bonds issued by Brazil. Hungary, Bolivia, China, Korea, Belarus are among the most overweight securities.

The highest-yielding ideas for EM Eurobond market

Mexico has been suffering from funds fleeing to Brazil and unpopular policies of the president-elect, though Brazil is lagging behind Mexico by four notches on the sovereign scale. However, if the new leader pushed ahead with his reforms, the rating is expected to go up by two notches, from BB+, narrowing the gap with the bottom investment-grade tier (ВВВ-). Mexico’s bonds (BBB+ composite rating) are the cheapest across EM on the sovereign curve, though the country will keep its investment-grade even if it is downgraded by S&P and Fitch.

However, the gap between corporate issues is wider, as, for instance, in the case of Pemex (BBB-). The company’s securities yield as much as the ВВ+/BB-rated bonds.

This is why our top picks among corporates come from Mexico’s fast-growing banking/finance bonds that remain the most underweight securities: Unifin (BB), Alpha B+, Findep (BB-) etc.

HY and other EM USD Eurobonds

Source: Bloomberg, ITI Capital

Source: Bloomberg, ITI Capital

Newest trade ideas

1) UNIFIN is largest non-regulated Mexican leasing company with over 25yrs of history, operating as a non-banking financial services company, specializing in three main business lines: operating leasing, factoring and auto and other lending. Its assets are estimated at 68bln Mexican peso($bln). Leasing composes 78% of company portfolio followed by autoloans 16% and factoring 5%. Loan portfolio and net income have grown at a ’16— ’18 CAGR of 31% and 26%, respectively strong profitability, with an average ROAE and ROAA of 23% and 3%, over the last 3 years Strong asset quality with leasing NPLs historically below 1% targets mainly the expanding SME segment.

Total leasing in Mexico to SME as % of GDP is the lowest in LATAM only 40%, while banking credit is 20%.

2) Financiera Independencia is Mexico’s largest micro finance provider with 20% share of the market amongst non-financial banking organisations. Lender to lower income segment individuals under the personal, payroll and group loans methodologies in Mexico. Mexico has large potential in sphere of domestic household lending due to low banking penetration and underserved personal loan segment. Current lending to domestic household is 32% which is second lowest in LATAM after Argentina 15% and vs 67% in Brazil, while in USA its 190%. Current NPL ratio at 5,5%.

Loan portfolio in 2018 grew by 4% yoy to 8,2 bln Mexican peso. In 4Q18 net income was MX$79.8 mm, 54.7% higher YoY and the third highest reported since 1Q15. This solid 4Q performance led to an accumulated net income of MX$262.1 mm, surpassing our expectations for the 2018 year. The Average Effective Lending Rate increased by 191 bps to 66.3% in 4Q18 versus 4Q17.The Average Funding Cost was 11.3%, 92 bps lower than in 4Q17, consistent with the extension on the average tenor of the company’s debt from 1 to 5 years. Equity to Total Assets of 34.7%, 37 bps higher than in 4Q17. ROAE in 4Q18 was 7.7%, versus 5.1% in 4Q17, 260 bps higher. NIM is the highest in the industry, over 50%.

3) Alpha Holding S.A. de C.V. is a non-operating holding company whose business is mainly focused on payroll discount lending to public employees and retirees in Mexico, as well as in Colombia. Total assets over 17bln mxn peso. NPL ratio us 3,3%. ROAE above 20% and NIM is just above 6%.

4) Helios Towers (HTA) owns and operates telecommunications towers and passive infrastructure in five high-growth African markets. leading independent telecoms tower company in Africa, and are market leaders in Tanzania, Democratic Republic of Congo («DRC») and Congo Brazzaville («Congo B»). We own a growing portfolio in Ghana, with a particular strength in high-traffic urban areas. Company also announced market entry into South Africa in January 2019 Revenue for the 12 months increased by 3% year-on-year to US$356.0m (FY 2017: US$345.0m).

Adjusted EBITDA up 22% year-on-year to US$177.6m (FY 2017: US$146.0m) with FY 2018 Adjusted EBITDA margin at 50% (FY 2017: 42%), up 8ppts. Q4 2018 Adjusted EBITDA up 13% year-on-year to US$46.5m (Q4 2017: US$41.1m) with Q4 2018 Adjusted EBITDA margin at 52% (Q4 2017: 46%), up 6ppts. Cash and cash equivalents of US$89.0m at the end of the year (FY 2017: US$119.7m). Highly leveraged, Net debt to EBITDA over 3x.

5) Omantel (BB+) is the first telecommunications company in Oman and is the primary provider of internet services in the country. The government of Oman owns a 51% share in Omantel. Revenue for FY 2018 recorded a growth of 2.6% compared to last year EBITDA & Net Profit is 38.2% and 13.9% respectively. Net Profit (excl Zain Dividend & Interest Cost) is higher than last year by 8%. Net debt to EBITDA has fallen in Q4 18 to below 3x from 3,2x in Q3 2018. 5.2% growth from Fixed Line Retail revenues compared to last year. 12.8% increase in Fixed Broadband revenue and Growth in Fixed Broadband subscriber by 11.8%. Mobile Retail revenues decreased by 4.7% compared to last year mainly due to decline pre-paid subscriber base/revenues.

6) Mallincrodt (22B+) Mallinckrodt Pharmaceuticals is an Irish—tax registered manufacturer of specialty pharmaceuticals (namely, Acthar), generic drugs and imaging agents, that generated 90% of 2017 sales from the U.S. healthcare system. While Mallinckrodt is headquartered in Ireland for tax purposes, its operational headquarters is in the U.S it performed well in Q4 18, with earnings up 8% year-over-year at $2.18. Overall, its quarterly revenues jumped by 5% to reach $834.9 million, while it had reported $792.3 million in the same period a year ago.

EM HY yield curve, %

Source: Bloomberg, ITI Capital